"Looks cool… Come back when you have a lead".

If you've ever raised funds, you heard that sentence dozens of times.

Most VCs don't want to be the first check in. They prefer waiting until a "lead investor" commits the first check, and then co-invest alongside them.

It sucks, and it throws founders into an infinite loop. How can you raise if nobody will commit first?

Today, we cover three strategies you can use to secure your lead investor. But before that, let's understand what a lead investor exactly does, and why nobody wants to be one.

Fair warning: there's no silver bullet. Fundraising is hard.

Table of Contents

I. Understand what a lead investor is

1. A lead investor commits first

When raising a priced round, the pivotal moment happens when an investor "commits" i.e gives you a term sheet.

Although not bulletproof, a term sheet is widely regarded as a commitment to invest, and will act as a hugely positive signal. "We have a term sheet from X" is truly a magic word.

Once you have a term sheet, the round usually fills up quickly with co-investors who follow the lead on the same terms. Fundraising is an asymmetrical process, and getting that first term sheet is 80% of the work.

In some cases, you may even have different VC firms compete to lead your round!

Congrats, that's a rare occurrence and you have some bargaining power. You can negotiate more favorable terms or even suggest that they co-lead your round.

2. A lead investor invests the largest share of the round

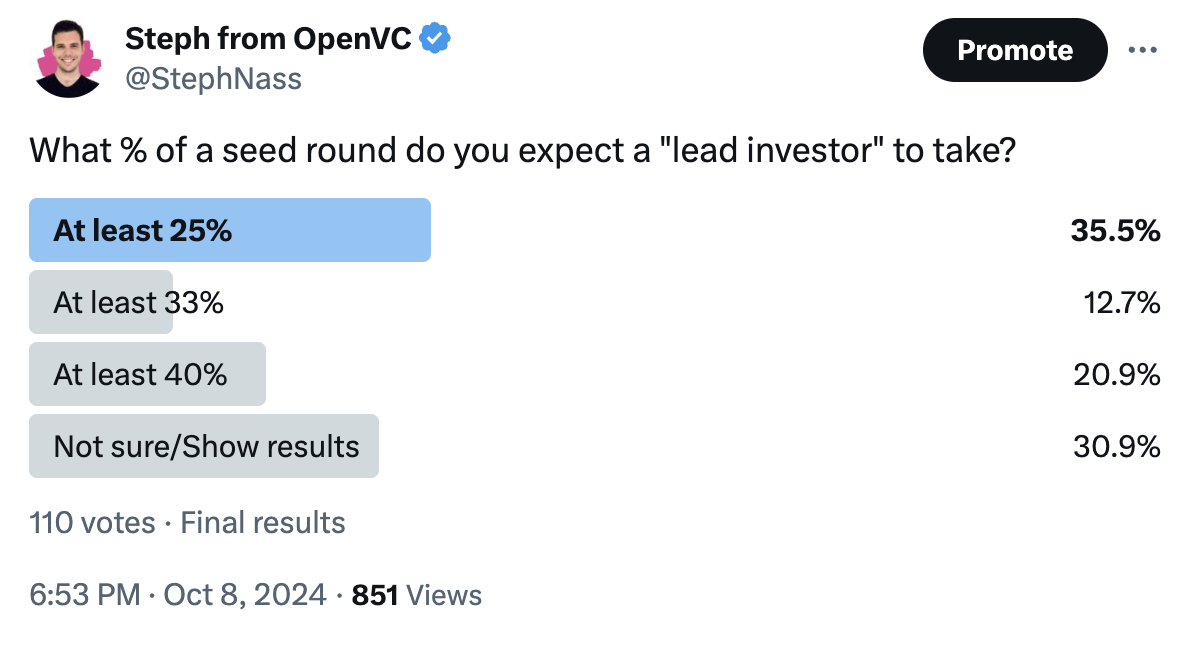

A lead investor doesn't just invest first, they also put down the largest check.

It can be as little as 20% of the round at the growth stage, but closer to 40% or 50% at the early stage, when the rounds are smaller.

So if you're raising a $2M seed, you're ideally looking for a $800k+ lead check.

3. A lead investor runs the due diligence and negotiate the terms

The lead investor has to do their own due diligence: going through your deck, combing your data room, browsing your finances, calling your customers, and spending time building conviction about the case.

For that reason, the lead investor is also the best positioned to negotiate the terms. Upon completing the due diligence, they know better than anyone else what the company is worth, and as importantly, how bad they want that deal.

So prepare yourself, you'll spend many hours on Zoom calls with your potential lead investor.

4. A lead investor may bring in other investors into the round

Unless the lead investor takes 100% of the round, you will need co-investors.

Armed with a fresh term sheet, you will certainly gather interest from other investors. But your lead may also bring in his own network to the party.

Venture capital is a social act. Being on a cap table is like joining a social club. It's common practice for a lead investor to help fill the round by bringing in their peers. Those co-investors may have a strategic value for you (potential lead for the next round, strategic value-add) and for your lead (basically getting or returning a favor).

5. A lead investor may take a board seat

Once the deal is closed, many VCs want to keep an eye on how things are going. Therefore, the lead investor may require a board seat.

An early-stage startup typically has 5 board seats or less, and they are not just for show. A board member has several powers, including voting rights for future funding and acquisitions, but also for hiring and firing executives. Yes, that includes the founders as well.

But a board member is also an asset, whereby the investor provides strategic advice, ensures the company is headed the right way, and supports the CEO in many ways.

II. Why nobody wants to lead rounds

Now that we've established the role and responsibilities of a lead investor, I'm sure you can see why nobody wants to lead.

1. Nobody wants to pay for the due diligence and legal fees

Leading a round is expensive.

The due diligence process takes dozens of work-hours from both analysts and partners, as well as copious fees from accountants, lawyers, and any other expert that may be required to build an educated opinion on the deal.

Keep in mind that a VC firm is a tiny company that lives off of their management fees. They rarely have armies of analysts to throw on your case.

Assuming the due diligence is successful, there's still more legal costs required to hammer out the legal paperwork and effectively close the deal.

When all is said and done, the cost to lead can range from $10k to $100k+.

(And by the way, if an investor asks you to pay the DD fees, it's probably a scam ).

2. Nobody has the expertise and coverage to tell what a great deal is

Let's say you're building the next 10X Genomics and reach out to biotech VCs.

How much do you think a random "biotech VC" knows about the genomics tooling market? Do they know the actual margins, the distribution channels, the idiosyncrasies of the buyers, the very specific supply chain, the multiple use cases? Do they know about that team in Singapore that's building a radically new approach to the problem? And do they know all of that well enough to make a multi-million dollar bet over the next 10 years?

Most VC firms have narrow domain expertise - typically related to the GP track record. They can lead within that spectrum, not much further.

And that's assuming they have enough coverage...

A VC once told me "Investing in a startup is like buying a house. You need to see tons of products before you know what you're looking for." If you only see 50% of the deals in your space, can you really make a good call? What if you only see 30%?

Therefore, the few VC firms with expertise and coverage tend to lead rounds, while the others follow due to insufficient information.

This drastically reduces the pool of lead investors.

3. Nobody has the guts to make a call on their own conviction

For investors, every deal they lead is a personal judgment.

At the end of the day, an investment decision always comes down to the investor's intuition, his or her talent.

Invest in a unicorn and you'll be remembered for that (see Jcal and Uber). Invest in a dud, and you're risking your social capital, including with your LPs.

So how do you save your face? By putting the blame on someone else! Co-invest with a big name VC and if things turn bad, well, tough luck.

III. The 3 ways to secure a lead investor

OK, now that we know what a lead investor is and why nobody wants to be one, how do you secure one for your own round?

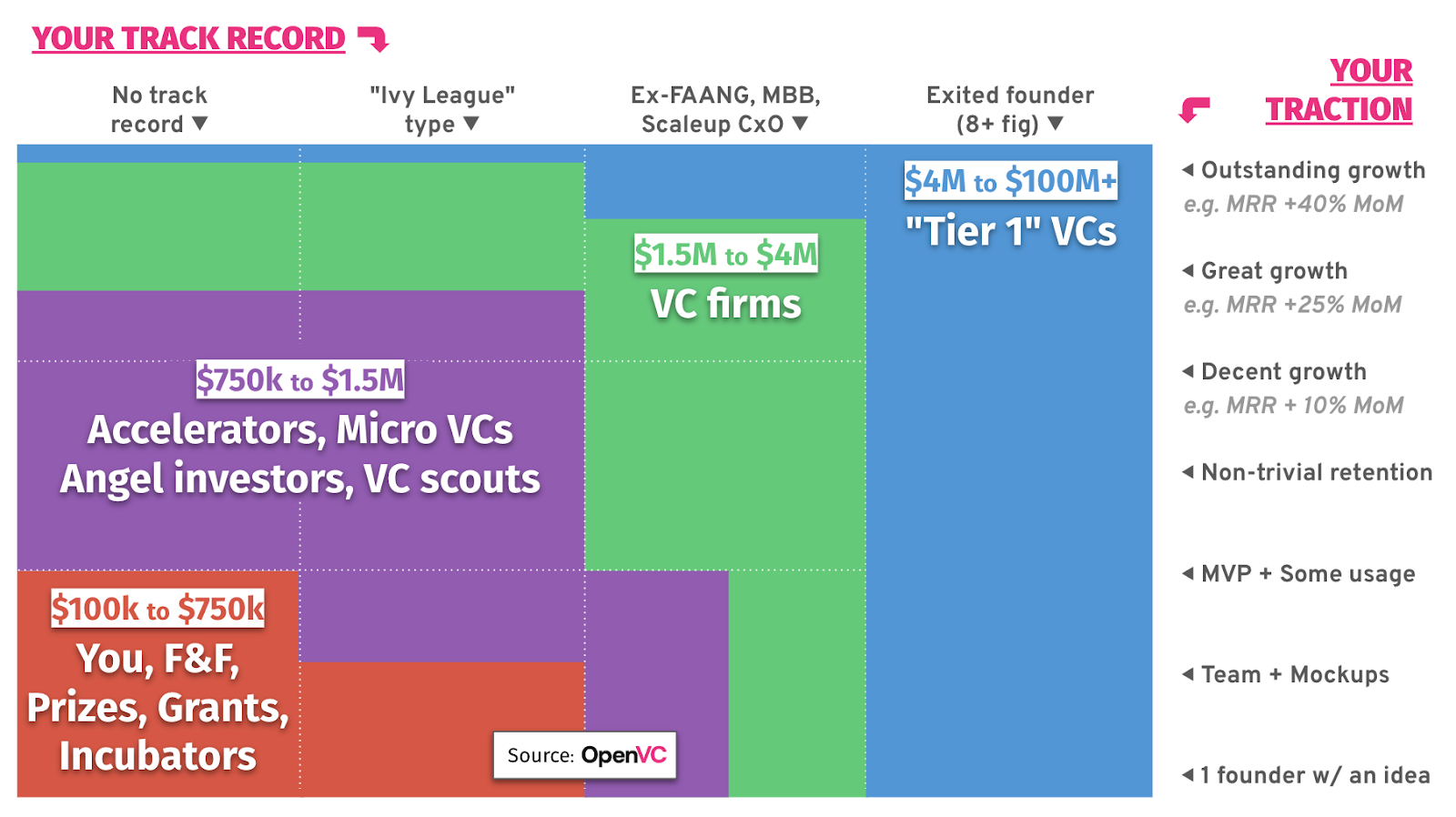

1. Ten years before: cultivate your track record and connections

This won't help most readers, but it must be said.

Experienced founders have spent their career in a specific market or industry. They have accumulated a successful track record and built up connections. Knowing VCs is just a natural side effect of that process.

A case in point - Jensen Huang, CEO of Nvidia, got his first check from Sequoia Capital thanks to a referral from his former boss Wilf Corrigan:

Some may consider this favoritism. I'd rather see it as years of hard work and talent being recognized.

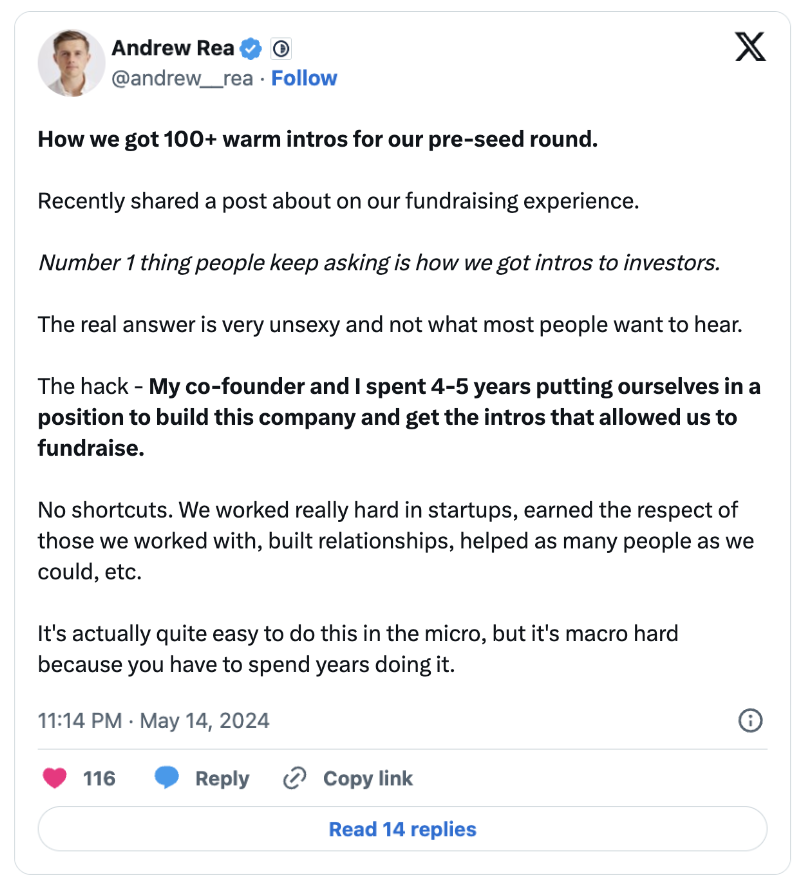

Andrew Rea recently shared his own example:

Andre sums it up pretty well: work hard alongside key people, get recognized for your worth by these "super-connectors", and when the time comes, you'll have access to capital.

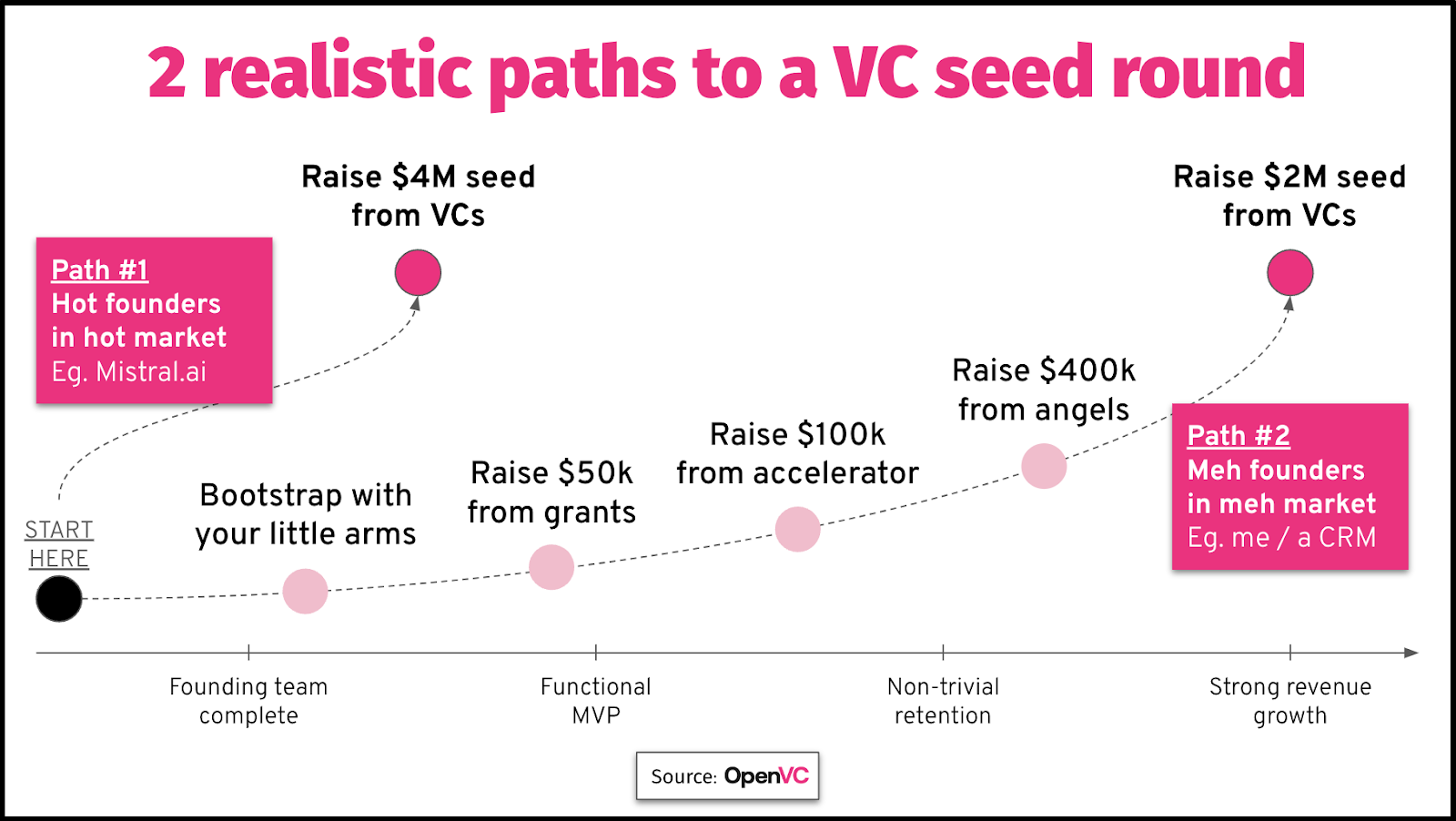

2. Two years before: build up a strong deal

VCs are always on the lookout for a great deal.

It might be an obvious thing to say, yet many founders don't understand what makes a deal "great". It's not about your market, your competition, or your passion - although these things matter. It's about traction. Show up with a top 1% deal in terms of traction, and you'll get a term sheet regardless of intros.

(Talking mostly for software companies here. Deeptech is different.)

However, no VC will fund that first phase (unless you have track record and network as mentioned before).

So you're on your own. You have to build up your company step by step, brick by brick, until you reach the traction level that will make a lead investor excited.

Realistically, it's a 2-plus-year journey where you bootstrap and raise small checks (angels, accelerators, F&F)...

See "Path #2" in the graph below.

3. Today: execute a flawless raise

Most founders are first-time founders. They have never raised funds before.

Therefore, many make beginner's mistakes: a terrible pitch deck, a nonsensical valuation, a ridiculous market sizing…

In most cases, this would be fine. After all, we're all here to learn and improve. However, this isn't true with fundraising. You only get one chance to make a good impression (if any...), so you need to bring your A game from the start.

There are so many ways to screw up your raise, and so little margin of tolerance!

So learn how to raise. It's a process that you can learn in a few hours. Start with our Fundraising strategy post, and from there, just follow the link.

I know many of you will ignore this advice. You just want to reach out to VCs ASAP.

You're wrong.

If you want to secure a lead investor, learn how to raise first. This will pay off hundredfold.

IV. Skip the lead, raise with SAFE instead

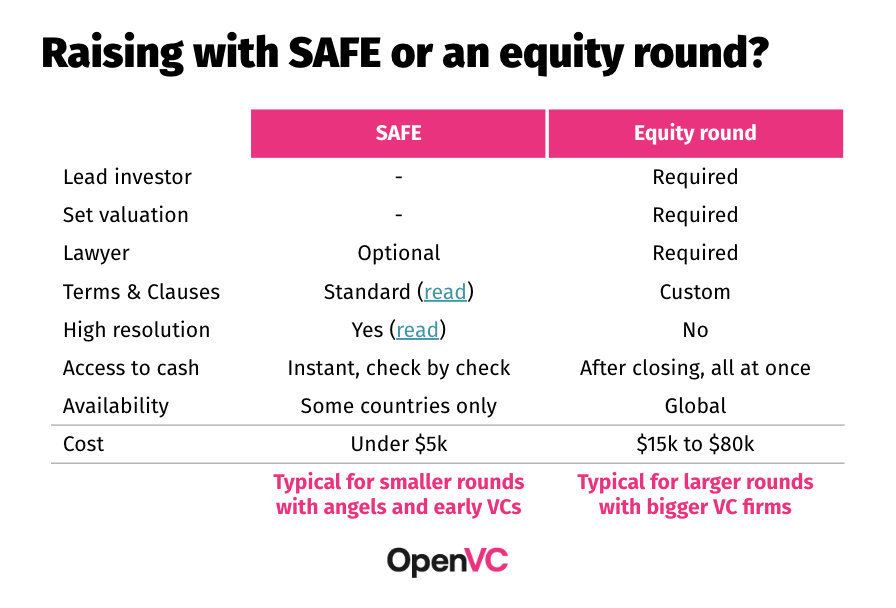

Did you know? You don't need a lead investor if you're raising with SAFE.

When discussing fundraising, most people think about a priced round, where you sell equity at a set valuation, with a lead investor setting the terms. This has been the default way to raise funds for the past few decades.

However, founders increasingly use SAFE instead of priced rounds. SAFE are great for their simplicity: if someone wants to invest, they just sign the doc and wire the money. No need for a lead!

Of course, SAFE are not perfect:

- SAFE are mostly used for smaller rounds, typically under $2M. Above that, most investors want a priced round, which gives more legal protection.

- Consequently, SAFE are mostly used by accelerators, angels, and very early VC firms. By using SAFE, you cut yourself from bigger VC firms.

- Some countries in the world don't have SAFE, or their tax system is set in a way that doesn't encourage using them (looking at you, Denmark…)

- You still need to convince people to invest! But at least, they cannot hide behind the excuse of "finding a lead".

So if you're raising less than $2M and that your jurisdiction allows it, consider using SAFE to solve the lead conundrum.

I hope this post gave your a better understanding of what a lead investor is, why nobody wants to be one, and a few directions to find yours.